With the recent budget impasse in Washington, it seemed like a prudent exercise to look at the fiscal regime in the American capital given the partial shutdown and federal budget issues that seem to appear on a fairly regular basis. As I have done in the past, let's look at how often Washington has suspended and raised the debt limit as well as invoking the use of "extraordinary measures" to ensure that the services provided by the federal government to taxpayers remain intact.

The modern debt limit was created in 1939 as the Public Debt Act of 1939 and was replaced with the Public Debt Act of 1941 (aka H.R. 2959 - 77th Congress) that set the stage for the financing of modern government debt financing. Here is the title page for the Act:

Until the 1941 act was passed, the federal government treated all interest and capital gains on its debt obligations as tax exempt. The 1941 act changed this by making the difference between the purchase and redemption price for savings bonds taxable. At the time that the Public Debt Act of 1941 was passed, the aggregate limit on all federal debt obligations was placed at $65 billion. Keeping in mind that the United States was about to enter the Second World War, this limit was raised as follows:

1942 - $126 billion

1943 - $210 billion

1944 - $260 billion

1945 - $300 billion

In 1946, the Public Debt Act was once again amended, lowering the debt limit to $275 billion.

Here is a lengthy table showing the entire history of changes to the debt limit:

Since the concept of a debt ceiling was launched in 1941, Congress has either changed, amended or suspended the statutory debt limit 121 times (up to and including 2017).

Here is a line graph showing the evolution of the debt ceiling since 1941 and how it is projected to grow out to 2023:

It is also important to note how the debt ceiling growth rate accelerated substantially just after the beginning of the new millennium as the War on Terror began and during the Great Recession when Washington spent trillions of taxpayers' dollars bailing out Wall Street and the banking sector as a whole.

Here is a detailed look at the period between 2010 and the beginning of 2018 showing how often Congress has had to rewrite its own debt laws:

At some point, Congress may find it difficult to kick the debt can further down the road, particularly in a scenario where Washington will find itself bailing out the economy as it did during the Great Recession. If we want a sense of what could lie ahead should Washington continue its overspending ways, here is a screen capture from the United States Department of Commerce showing the federal government services that will remain active during the most recent lapse of Congressional appropriations:

Here is a list of the services that will not be available during the funding lapse:

Obviously, the longer that the federal government is underfunded, the more services that will have to be reduced since the government cannot run on ether.

The current level of political polarization in Washington has very effectively accomplished one thing; it has made American voters forget all about the fiscal mismanagement that has taken place, an issue that will eventually cost American taxpayers hundreds of billions of dollars in annual interest payments on the debt that Washington has accumulated over the past two decades in particular.

On December 20, 2018, Russia's President Vladimir Putin held his annual press conference, his fourteenth and first of his new term in office. The event was held at Moscow's World Trade Center and ran for nearly 3 hours and 45 minutes. This year, the event was attended by a record 1700 journalists from Russia, Asia, Europe and the United States, up from 1640 in 2017.

Hereis a link to the entire annual press conference which is translated into English:

Hereis a link to the English language transcript of the press conference.

President Putin began by outlining Russia's economic data for the first nine months of 2018, noting that the nation's unemployment rate is expected to drop from a record low of 5.2 percent in 2017 to 4.8 percent in 2018. Russia's trade balance is expected to reach $190 million in 2018 ($157 million in the first three quarters of 2018) and the nation's gold and foreign currency reserves have grown by over 7 percent to $464 billion. For the first time since 2011, Russia will have a federal budget surplus of 2.1 percent of GDP, in contrast, the United States ran a budget deficit of 3.9 percent of GDP in fiscal 2018. This is a dramatic improvement from the early 2000s when the deficit was about 3 percent of GDP and the non-oil-and-gas deficit was 13 percent in 2009.

Let's look at some of Mr. Putin's comments on key issues that have made headline news in the West over the past year.

Given the ongoing sanctions that have been wielded by the West to punish Russia over its moves in Crimea, I found these comments in reference to Russia's present and future economic growth interesting and how Russia is planning for the future:

"By the way, you mentioned the projected 2 percent growth for the next two years. Yes, in the next years, 2019–2020, two percent each, but from 2021, the Government is already planning 3 percent, and then more. Therefore, I strongly hope that we will manage to do all this. Some fluctuations are probably possible, but, I repeat, the most important thing is that we need… Do you see what we need to do?We need to join another league of economies,and not only in terms of volumes. I think that taking the fifth place in terms of volume is quite possible. We used to rank fifth in terms of the economy, in purchasing power parity, and we will do it again, I think. However, we need to ascend to another league in terms of the quality of the economy. This is what our national projects are aimed at....

After all, we need to talk about bilateral relations; we are interested in this, as well as our American partners are, by the way. Of course, there is no super-global interest.Our mutual trade stands at a meagre 28 billion, or even lower now, less than 28, 25 to 27 billion maybe. This is nothing, zero. With China, we will reach 100 billion this year, and with the US, everything is in decline.Who is interested in this? No one, not even the President of the United States, who is promoting the idea of reviving the economy, as he says, in his quest to make America great again."(my bold)

As we've seen, both China and Russia are both working to diversify their international trading partnerships. By working around trade with the United States (i.e. joining another league of economies), Russia can blunt the impact of American-led and American-driven economic sanctions.

Here is an interesting exchange about the potential for nuclear war and Russia's response to the United States withdrawal from the INF Treaty. When reading this section, it is important to keep in mind that the Soviet Union lost at least11 million soldiers and between 7 and 20 million civiliansduring the Second World War. By comparison, the United States lost roughly 400,000 soldiers and almost no civilians. As well, while entire major cities in Russia were both besieged and levelled, not a single bomb was dropped on the United States:

"Anton Vernitsky:Mr President, as Soviet-era children, all of us feared a nuclear war very much. As you remember, various songs dealt with this issue. One of them had the following lyrics: “Sunny world: Yes, yes, yes; nuclear explosion: No, no, no.”

Vladimir Putin: Are you not afraid today?

Anton Vernitsky: Forty years have passed, and major media outlets on both sides of the ocean are beginning to publish a scenario for a nuclear exchange between Russia and the United States. The word “war” is sounding more and more often at household level, in kitchens.

Mr President, how can you calm down my little son who, just like me, also fears a nuclear war today? What words and actions can calm us all down?

Vladimir Putin: You know, I think you are right.

I just thought that all this, including the danger of such developments in the world, is now being hushed up and played down to some extent. It seems impossible or something that is not so important. At the same time, if, God forbid, something like this happens, it might destroy the whole of civilisation or perhaps the entire planet.

These issues are therefore serious, and it is a great pity that there is such a tendency to underestimate the problem, and that this tendency is probably becoming more pronounced.What are the current distinguishing features and dangers?

First, all of us are now witnessing the disintegration of the international system for arms control and for deterring the arms race.This process is taking place after the United States withdrew from the Anti-Ballistic Missile (ABM) Treaty that, as I have already noted a thousand times, was the cornerstone in the sphere of non-proliferation of nuclear weapons and deterring the arms race.

After that, we were forced to respond by developing new weapons systems that could breach these ABM systems. Now, we hear that Russia has gained an advantage. Yes, this is true. So far, the world has no such weapons systems. Leading powers will develop them, but, as yet they do not exist.

In this sense, there are certain advantages. But, speaking of the entire strategic balance, this is just an element of deterrence and for equalising parities. This is just the preservation of parity, and nothing more.

They are now about to take another step and withdraw from the INF Treaty. What will happen? It is very difficult to imagine how the situation will unfold. What if these missiles show up in Europe? What are we supposed to do then?

Of course, we will need to take some steps to ensure our safety. And they should not whine later that we are allegedly trying to gain certain advantages. We are not. We are simply trying to maintain the balance and ensure our security.

The same goes for the START III Treaty, which expires in 2021. There are no talks on this issue. Is it because no one is interested, or believes it is necessary? Fine, we can live with that.

We will ensure our security. We know how to do it. But in general, for humanity, this is very bad, because this takes us to a very dangerous line.

Finally, there is another circumstance I cannot ignore. There is a trend to lower the threshold for the use of nuclear weapons. There are plans to create low-impact nuclear charges, which translates to tactical rather than global use. Such ideas are coming from Western analysts who say it is okay to use such weapons. However, lowering the threshold can lead to a global nuclear disaster. This is one danger we are facing today.

However, I believe humanity has enough common sense and enough of a sense of self-preservation not to take these things to the extreme." (my bolds)

With the news that the United States was withdrawing its forces from Syria now that it had accomplished its mission of destroying the Islamic State, Rachel Marsden from the Chicago Tribune asked the following questions:

"Yesterday, President Donald Trump announced the withdrawal of the American troops from Syria. He also announced that, in his opinion, the United States defeated ISIS in Syria, he made that very clear.

What is your position with respect to his statements, both on the withdrawal of the American troops from Syria and also with his statement regarding the defeat of ISIS by the United States?

And, secondly, do you have concern that the American troops will remain in some form? There has been much discussion, for example, around the presence, potentially, of contractors in other jurisdictions where the United States is either out of militarily or might want to be out of militarily but in a more discreet way."

Here is Mr. Putin's response:

"As concerns the defeat of ISIS, overall I agree with the President of the United States. I already said that we achieved significant progress in the fight against terrorism in that territory and delivered major strikes on ISIS in Syria.

There is a risk of these and similar groups migrating to neighbouring regions and Afghanistan, to other countries, to their home countries, and they are partly returning.

It is a great danger for all of us, including Russia, the United States, Europe, Asian countries, including Central Asia. We know that, we understand the risk fully. Donald is right about that, and I agree with him.

As concerns the withdrawal of American troops, I do not know what that is. The United States have been present in, say, Afghanistan, for how long? Seventeen years, and every year they talk about withdrawing the troops. But they are still there.This is my second point....

Is the presence of American troops required there? I do not think it is.However, let us not forget that their presence, the presence of your troops, is illegitimate as it was not approved by a UN Security Council resolution. The military contingent can only be there under a resolution of the UN Security Council or at the invitation of the legitimate Syrian Government. Russian troops were invited by the Syrian Government. The United States did not get either of these so if they decide to withdraw their troops, it is the right decision." (my bolds)

Even the United States is concerned about the migration of tens of thousands of potential terrorists as I wrote in this posting.

Here is Mr. Putin's solution to the "Syria problem":

"The current issue on the agenda is building a constitutional committee.

By the way, when we met in Istanbul – I mean Russia, Turkey, France and Germany – we agreed to make every possible effort to create this constitutional committee and Russia, for its part, has done everything in its power for this to happen.

As strange as it may seem, we fully agreed on the list of members with President al-Assad, who designated 50 people and was involved in selecting 50 more from civil society. Despite the fact that he is not happy with everything, he agreed with this.

Turkey, which represents the interests of the opposition, also agreed. Iran agreed. We submitted the list to the UN and, as Minister Lavrov reported to me just yesterday, unexpectedly, prompted by our partners – Germany, France and the United States – UN representatives (Mr de Mistura) decided to wait and see.

I do not understand what is going on there but at any rate, I want to believe that this work is in its final stage. Maybe not by the end of this year but in the beginning of the next the list will be agreed and this will open the next stage of the settlement, which will be political settlement.

Here is a rather interesting exchange regarding Russia's place in the world:

Ann Maria Simmons: I want to know if you really want this. Also, please, what is the real goal of your foreign policy? Thank you.

Vladimir Putin:With regard to ruling the world, we know where the headquarters that is trying to do so is located, and it is not in Moscow. However, this is related to the leading role of the United States in the global economy and defence spending: the United States is spending over $700 billion on defence, while we spend only $46 billion.

Just think of it, we have 146 million people in Russia, whereas the NATO countries’ population is 600 million, and you think our goal is to rule the world? This is a cliché imposed on public opinion in Western countries in order to resolve intra-bloc and domestic political issues.

When I say intra-bloc, I mean that in order for NATO to rally countries around itself, it needs an external threat. It does not work otherwise. You have to have someone to rally against. As a major nuclear power, Russia fits the bill perfectly...

In fact, the main goal of our foreign policy is to provide favourable conditions for the Russian Federation, its economy and social sphere, to ensure unfettered movement forward and to strengthen our country from the inside, above all, so that it can take its rightful place in the international arena as an equal among equals.

We are in favour of consolidating the system of international law, ensuring unconditional compliance with the UN Charter, and using this platform to develop equal relations with all the participants of international affairs."

Let's close this posting with a look at what Mr. Putin had to say about the situation regarding Crimea, the main reason why the United States and its European lapdogs imposed sanctions on Russia:

Artyom Artemenko (Crimea 24 television network): Mr President, you recently said that the restrictions Russia is facing from some countries have a direct bearing on the people living in Crimea who voted for reunification with Russia in 2014. Can you explain what you meant? How do we deal with this? Thank you.

Vladimir Putin: I did say this, even though I can hardly recall where I was at the time, but I can explain it. This is an interesting situation.What we hear from the outside is that Russia annexed Crimea. But what does annexation mean? It means a forcible takeover. If this had been an annexation and a takeover by force, the people in Crimea would have had nothing to do with it and would not be to blame. But if they came out and voted, this was not an annexation.So what is going on? After all, sanctions were imposed against them, against you. What are these sanctions? Restriction on mobility, restrictions on border crossings, visas, financial transactions, insurance companies, marine infrastructure use and the use of other facilities. These measures affect almost everyone living there. They were the ones targeted by these sanctions, and this is not just about singling out specific individuals like the government leaders in the Republic of Crimea and Sevastopol, but about targeting everyone. If they had had nothing to do with it, if it had been annexation, why were the people sanctioned? But if you were sanctioned for taking part in a specific vote, then they would have to admit that it actually took place. This is what this is about, and this is what I meant."

While you may not necessarily believe what Mr. Putin has to say, you must ask yourself this question:

When was the last time that the political leader of your nation sat down for nearly 3 hours in a question and answer session and had an audience of 1700 journalists? Despite whatWestern media says, Mr. Putin's approval rating is still the envy of most of the West's elected leadership as shownhere:

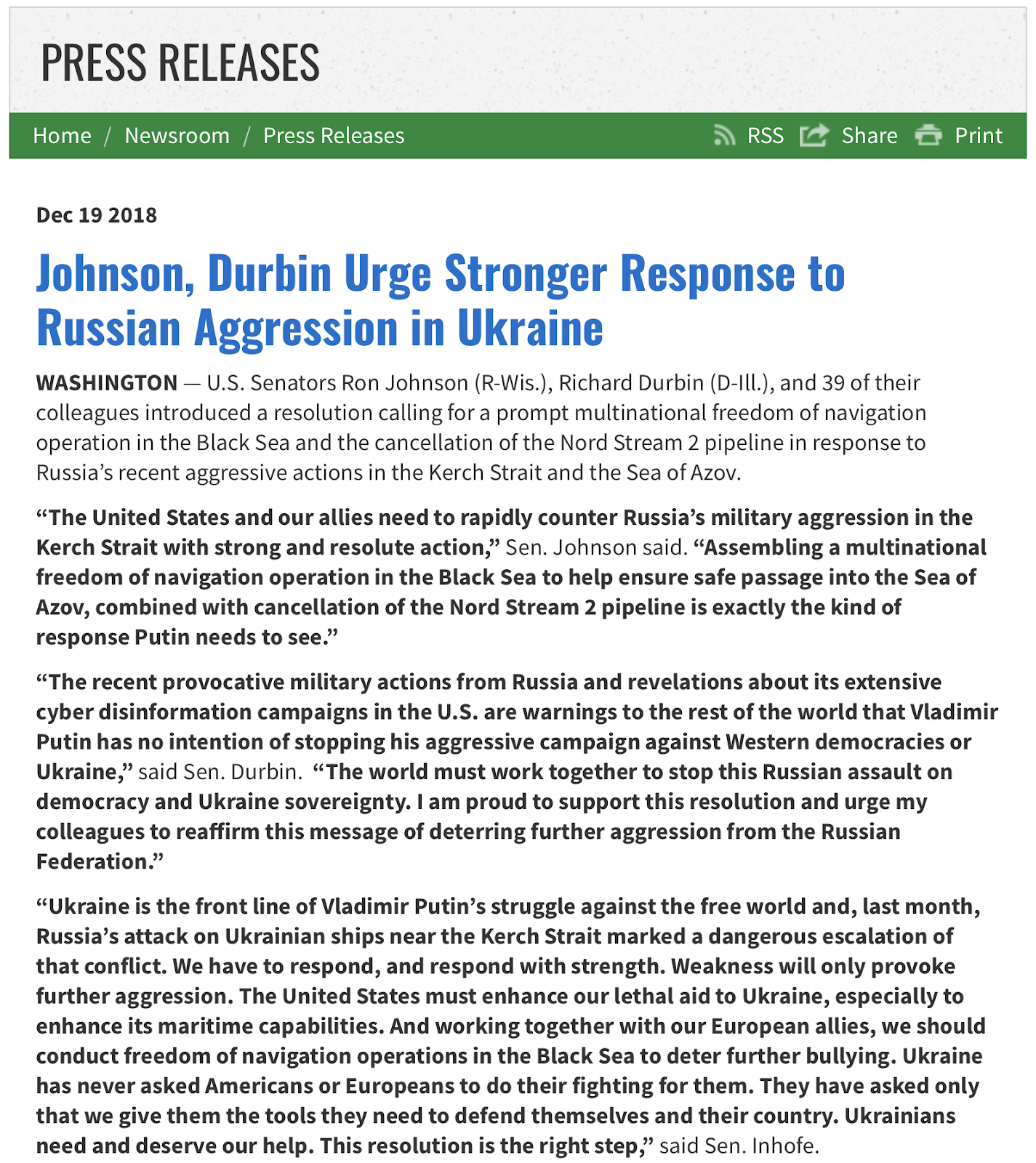

While the rest of us are distracted while we firm up our Christmas plans and finishup the last minute shopping that we are all prone to do, the United States Senate has been busy on another front; taking measures that could well lead to a hot war with Russia given the recent international incident between Russia and Ukraine in the Kerch Strait.

Senator Ron Johnson (R- Wis) and Richard Durban (D-Ill) and 39 of their colleagues introduced a Senate Resolution on December 19, 2019 which calls for "a prompt multinational freedom of navigation operation in the Black Sea and urging the cancellation of the Nord Stream 2 pipeline" as shown here:

Here is a list of co-sponsors of the resolution:

Sen. James Inhofe (R-Ok.), chairman of the Senate Armed Services Committee; Sen. Chris Murphy (D-Conn.), ranking member of the Senate Foreign Relations Subcommittee on Europe and Regional Security Cooperation; and Sens. John Barrasso (R-Wyo.), Ben Cardin (D-Md.), Marco Rubio (R-Fla.), Jeanne Shaheen (D-N.H.), Cory Gardner (R-Colo.), Christopher Coons (D-Del.), James Risch (R-Idaho), Richard Blumenthal (D-Conn.), Cindy Hyde-Smith (R-Miss.), Tammy Baldwin (D-Wis.), Sheldon Whitehouse (D-R.I.), Ben Sasse (R-Neb.), Johnny Isakson (R-Ga.), John Boozman (R-Ark.), John Hoeven (R-N.D.), Joe Donnelly (D-Ind.), Amy Klobuchar (D-Minn.), Jon Kyl (R-Ariz.), Thom Tillis (R-N.C.), Doug Jones (D-Ala.), Roy Blunt (R-Mo.), Mike Rounds (R-S.D.), Heidi Heitkamp (D-N.D.), Maggie Hassan (D-N.H.), Tim Kaine (D-Va.), Joe Manchin (D-W.Va.), Gary Peters (D-Mich.), Debbie Stabenow (D-Mich.), Tom Cotton (R-Ark.), Roger Wicker (R-Miss.), John Cornyn (R-Texas), John Thune (R-S.D.), Mazie Hirono (D-Hawaii), Mike Crapo (R-Idaho), Rob Portman (R-Ohio), Mitch McConnell (R-Ky.), and Tammy Duckworth (D-Ill.).

Here is the resolution (currently unnumbered) in its entirety:

Let's look at a map showing the key geographical components of the Black Sea and Sea of Azov region:

This map is somewhat outdated since the Crimean peninsula is now part of Russia following the March 2014 referendum which, despite receiving overwhelming support for Crimean independence from Ukraine has been viewed by the United States as an annexation by Russia. As you can see, Kerch (Kirch) Strait is the narrow waterway that connects the Black Sea to the Sea of Azov. It is this narrow body of water that Ukrainian artillery ships and tugboat sailed through, resulting in their apprehension by the Russian Navy as shown here:

The Sea of Azov borders on two nations; Russia to the east and Ukraine to the west. The Sea of Azov is of critical importance to Ukraine since it gives eastern Ukraine (i.e. Donetsk and Luhansk), which is now in the hands of non-government forces, access to marine passage.

Whether you believe that Russia or Ukraine has international marine law on its side is important, however, what is of a far greater concern is the entry of a third party into this tense situation. That is exactly what the Senate Resolution proposes through several mechanisms:

1.) the United States should promptly head up a robust multi-national (i.e. NATO) freedom of navigation operation in the Black Sea to demonstrate support for internationally recognized borders and bilateral agreements and to ensure that there is safe passage through the Kerch Strait by pushing back against excessive Russian claims of sovereignty.

2.) NATO should enhance its maritime presence and capabilities to support freedom of navigation in the Black Sea region.

3.) the President should use his authority under the National Defense Authorization Act of 2018 to enhance the capability of Ukraine's military.

4.) the President should use the Departments of Defense and State to provide additional security assistance to Ukraine, particularly to strengthen its maritime capabilities to defend itself and deter further Russian aggression.

5.) the President should imposed further mandatory sanctions against Russia under the Countering America's Adversaries Through Sanctions Act and inform Russia that these sanctions will remain in place until there is "an appropriate change in behaviour".

6.) the United States and its allies in Europe should deny Russian Navy vessels access to their ports for refuelling and resupplying.

As I have done in past postings, let's look at international maritime law as quoted from the United Nations Convention on the Law of the Sea which was signed into law on December 10, 1982. which allows innocent passage through bodies of water:

"1. Passage is innocent so long as it is not prejudicial to the peace, good order or security of the coastal State. Such passage shall take place in conformity with this Convention and with other rules of international law.

2. Passage of a foreign ship shall be considered to be prejudicial to the peace, good order or security of the coastal State if in the territorial sea it engages in any of the following activities:

(a) any threat or use of force against the sovereignty, territorial integrity or political independence of the coastal State, or in any other manner in violation of the principles of international law embodied in the Charter of the United Nations;

(b) any exercise or practice with weapons of any kind;

(c) any act aimed at collecting information to the prejudice of the defence or security of the coastal State;

(d) any act of propaganda aimed at affecting the defence or security of the coastal State;

(e) the launching, landing or taking on board of any aircraft;

(f) the launching, landing or taking on board of any military device;

(g) the loading or unloading of any commodity, currency or person contrary to the customs, fiscal, immigration or sanitary laws and regulations of the coastal State;

(h) any act of wilful and serious pollution contrary to this Convention;

(i) any fishing activities;

(j) the carrying out of research or survey activities;

(k) any act aimed at interfering with any systems of communication or any other facilities or installations of the coastal State;

(l) any other activity not having a direct bearing on passage." (my bold)

The Convention defines innocent passage as follows:

"The Convention retains for naval and merchant ships the right of "innocent passage" through the territorial seas of a coastal State. This means, for example, that a Japanese ship, picking up oil from Gulf States, would not have to make a 3,000-mile detour in order to avoid the territorial sea of Indonesia, provided passage is not detrimental to Indonesia and does not threaten its security or violate its laws....

At the Third United Nations Conference on the Law of the Sea, the issue of passage through straits placed the major naval Powers on one side and coastal States controlling narrow straits on the other. The United States and the Soviet Union insisted on free passage through straits, in effect giving straits the same legal status as the international waters of the high seas. The coastal States, concerned that passage of foreign warships so close to their shores might pose a threat to their national security and possibly involve them in conflicts among outside Powers, rejected this demand.

Instead, coastal States insisted on the designation of straits as territorial seas and were willing to grant to foreign warships only the right of "innocent passage", a term that was generally recognized to mean passage "not prejudicial to the peace, good order or security of the coastal State". The major naval Powers rejected this concept, since, under international law, a submarine exercising its right of innocent passage, for example, would have to surface and show its flag - an unacceptable security risk in the eyes of naval Powers. Also, innocent passage does not guarantee the aircraft of foreign States the right of overflight over waters where only such passage is guaranteed.

In fact, the issue of passage through straits was one of the early driving forces behind the Third United Nations Conference on the Law of the Sea, when, in early 1967, the United States and the Soviet Union proposed to other Member countries of the United Nations that an international conference be held to deal specifically with the entangled issues of straits, overflight, the width of the territorial sea and fisheries.

The compromise that emerged in the Convention is a new concept that combines the legally accepted provisions of innocent passage through territorial waters and freedom of navigation on the high seas. The new concept, "transit passage", required concessions from both sides.

The regime of transit passage retains the international status of the straits and gives the naval Powers the right to unimpeded navigation and overflight that they had insisted on. Ships and vessels in transit passage, however, must observe international regulations on navigational safety, civilian air-traffic control and prohibition of vessel-source pollution and the conditions that ships and aircraft proceed without delay and without stopping except in distress situations and that they refrain from any threat or use of force against the coastal State. In all matters other than such transient navigation, straits are to be considered part of the territorial sea of the coastal State."

I'll leave it up to my readers to determine whether Ukraine's passage through the Kerch Strait should be considered "innocent" under international law.

Let's close with a key extract from Senator Johnson's press release:

"Ukraine is the front line of Vladimir Putin’s struggle against the free world and, last month, Russia’s attack on Ukrainian ships near the Kerch Strait marked a dangerous escalation of that conflict. We have to respond, and respond with strength. Weakness will only provoke further aggression. The United States must enhance our lethal aid to Ukraine, especially to enhance its maritime capabilities. And working together with our European allies, we should conduct freedom of navigation operations in the Black Sea to deter further bullying." (my bold)

Here is a suggestion. Why don't we load Senator Johnson and his 40 colleagues onto a United States Navy ship and ensure that they actually get first hand experience of what a hot war with Russia will look like? Perhaps if they perceived that they were cannon fodder in a no-win war between the United States/NATO and Russia they would feel a bit different about this proposed resolution which is only serves to heat up the Cold War Part 2.

In its recentFinancial Stability Report, the Federal Reserve looks at the resiliency of the American economy and the key financial vulnerabilities that increase the level of risk for the economy as a whole, most of which are, in some way, connected to higher interest rates. This "navel gazing" by the Fed is fascinating, particularly given that it was the central bank's policies that led to the financial crisis and near collapse of the global economy between 2007 and 2009. While the Fed touts its success at reviving the economy since that time through the use of imaginative and untested monetary policies, it notes the following vulnerabilities that may have or already have "built over time":

• Valuation pressures are generally elevated, with investors appearing to exhibit a high tolerance for risk-taking, particularly with respect to assets linked to business debt.

• Borrowing by households has risen roughly in line with household incomes . However, debt owed by businesses relative to gross domestic product (GDP) is historically high, and there are signs of deteriorating credit standards .

• The nation’s largest banks are strongly capitalized, and leverage of broker-dealers is substantially below pre-crisis levels. Insurance companies have also strengthened their financial position since the crisis.

• Funding risks in the financial system are low relative to the period leading up to the crisis . Banks hold more liquid assets, and money market mutual funds are less vulnerable to destabilizing runs by investors

In this posting, I will focus on the issue of business debt since it is my personal belief that this is the Achilles heel of the American economy.

According to data provided by the Fed, this is what has happened to corporate bond yields for both BBB rated and high-yield (i.e. junk debt) since the mid-1990s:

As you can see, corporate bond yields have been at historical lows since the Great Recession and have only begun to move up during the last half of 2018 as the Fed has pushed interest rates higher.

What is even more concerning is the fact that investors have been lulled into believing that corporate debt is a secure investment as shown on this graphic which measures the spread between corporate debt and supposedly risk-free Treasuries:

What this graphic does not show is the fact that corporate bondholders are willing to extend loans to Corporate America with fewer credit protections to high-risk borrowers, a factor that could prove to be extremely painful to corporate bondholders should corporations start to default on their debt.

Now, let's look at how much businesses have borrowed. Here is a table showing the breakdown of business credit as well as total private nonfinancial credit (i.e. including household debt of all types) and the growth rates from Q2 2017 to Q2 2018 and the annual growth rate from 1997 to 2018:

Business debt makes up 49.14 percent of all private nonfinancial debt in the United States. Business debt has grown at 4.5 percent over the past year (measured from Q2) and 5.7 percent annually since 1997. What is more concerning is the growth in business debt relative to the size of the economy as measured using GDP:

Unlike household debt, business debt is now at historically high levels when measured against GDP.

Here is a graphic showing the issuance of riskier forms of business debt (leveraged loans and high-yield or junk bonds) going back to 2005:

While the issuance of risky debt dropped during 2015 to 2017, it has since picked up substantially and now totals more than $2 trillion.

In addition, credit standards for some business loans have deteriorated over the past six months. The share of newly issued large loans to companies with high leverage (ratios of debt to EBITDA greater than 6) exceeds levels seen in both 2007 and 2014 as shown here (coloured light brown on the bar graph):

As of the second quarter of 2018, around 35 percent of all corporate bonds outstanding were at the lowest end of the investment-grade group, totalling $2.25 trillion. Here's what the Fed has to say about this looming problem:

"In an economic downturn, widespread downgrades of these bonds to speculative-grade ratings could induce some investors to sell them rapidly, because, for example, they face restrictions on holding bonds with ratings below investment grade. Such sales could increase the liquidity and price pressures in this segment of the corporate bond market."

Given that, over the past year, firms with high leverage, high interest expense ratios and low earnings and cash holdings have been increasing their debt loads the most as shown on this graphic:

...we can clearly see where the next debt crisis in the United States is likely to occur, particularly as interest rates continue to rise.

In large part, the looming business debt problem in the United States was created by the Federal Reserve through its extended experiment with ultra-low interest rates. Unfortunately, a decade of low interest rates have lulled investors who are desperately seeking yield into a false sense of security, believing that a repetition of the Great Recession will never happen and that their investments in junk corporate debt will always retain their value.

I have been an avid follower of the world's political and economic scene since the great gold rush of 1979 - 1980 when it seemed that the world's economic system was on the verge of collapse. I am most concerned about the mounting level of government debt and the lack of political will to solve the problem. Actions need to be taken sooner rather than later when demographic issues will make solutions far more difficult. As a geoscientist, I am also concerned about the world's energy future; as we reach peak cheap oil, we need to find viable long-term solutions to what will ultimately become a supply-demand imbalance.